Egan-Jones CLO* Summary Report (January 2025)

*All Egan-Jones ratings in this report are non-NRSRO ratings

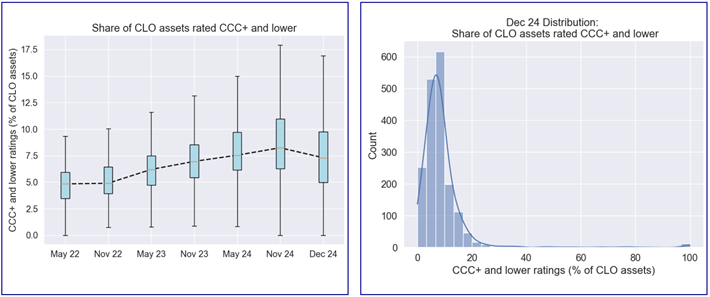

Better credit quality but tempering spreads - While CLOs issued in Dec. rose from 29 ($12.0B) in 2023 to 94 ($41.5B) in 2024, it was a decline from Nov. 2024’s print of 128 ($54.6B) (see Finsight.com)¹. The striking feature of the chart to the below right is the decline (i.e., rolling over) of rates on both the asset and liability side over the past several months, which has recently tempered. The major concern has shifted from credit quality to sustaining prior strong yields. As can be seen in chart I-D, the distribution of the CCC+ or lower assets has decreased along while WARS has improved slightly. (view all Egan-Jones CLO ratings)

Currently, Egan-Jones tends to have a more positive view of CLO credit quality as compared to other credit rating agencies, as demonstrated in the table below.

I. Deal Key Metrics Summary

As of December 2024, Egan-Jones rated 1835 CLO deals. We collected and calculated available deal level, tranche level and asset level key metrics such as deal weighted average rating factor and tranche subordinations, compared with prior period(s) analysis results and summarized highlights below.

I-A. Weighted Average Rating Score

Egan-Jones collected the weighted average rating score (WARS)³ of covered CLO deals. The 25th, 50th, and 75th percentiles of the WARS value were 3652, 3764, and 3899, respectively.

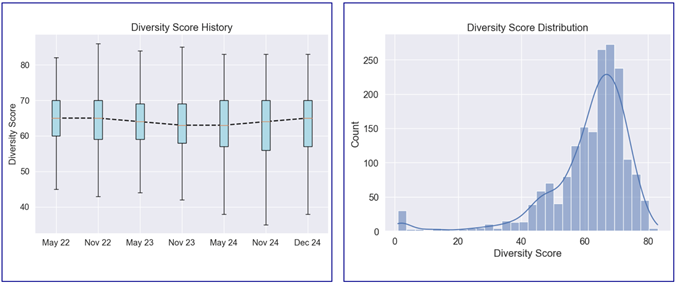

I-B. Diversity Score

Egan-Jones collected the Diversity Score (DS)⁴ of covered CLO deals. The 25th, 50th, and 75th percentiles of the DS value were 57, 65, and 70, respectively.

I-C. Super Senior Tranches Subordination

Egan-Jones collected the senior tranches subordination⁵ (%) (STS) of covered CLO deals. The 25th, 50th, and 75th percentiles of the STS value were 34.7, 36.1, and 38.5, respectively.

I-D. CCC+ or Lower Rating Percentage

Egan-Jones collected the CCC+ and Lower Rated Asset Percentage (%) (CLRA) of covered CLO deals. The 25th, 50th, and 75th percentiles of the CLRA value were 5.0, 7.3, and 9.8, respectively. Egan-Jones calculated and compared the monthly average value of CLRA data from May 2022 to this month. The mean value of CLRA has increased over the observed period, which indicates the percentage of lower rated assets might be increasing.

I-E. CLO Leverage Summary

Note: Deal balance is the sum of the current balance of all deal tranches; Debt balance is the sum of the current balance of all debt tranches.

Egan-Jones reviewed various liability/asset metrics. The 25th, 50th, and 75th percentiles of the total deal balance to collateral balance (total current tranches balance / current collateral balance) were 94.0%, 98.0%, and 99.0%, respectively. The 25th, 50th, and 75th percentiles of the debt balance to collateral balance (current non-equity tranches balance / current collateral balance) were 105.0%, 108.0%, and 110.0%, respectively.

II. Tranche Key Metrics Summary

II-A. Tranche Subordination Analysis

The average subordination levels (defaulted assets are valued at market value) of senior tranches and mezzanine tranches were 38.7% and 16.0%, respectively. The 25th, 50th, and 75th percentiles of senior tranche subordination levels (defaulted assets are valued at market value) were 34.8%, 36.2%, and 38.3%, respectively. The 25th, 50th, and 75th percentiles of mezzanine tranche subordination levels (defaulted assets are valued at market value) were 8.8%, 15.0%, and 22.2%, respectively.

The mean, 25th, 50th, and 75th percentiles of the available subordination of each rating category (includes +/-) can be found in the table above.

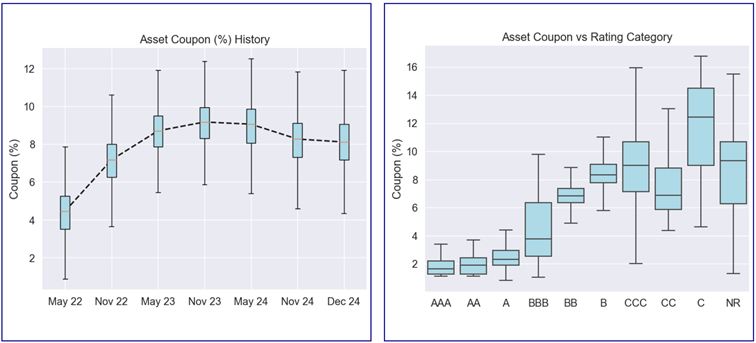

II-B. Tranche Coupon Analysis

The average coupon of senior tranches and mezzanine tranches are 5.9% and 8.2%, respectively. The 25th, 50th, and 75th percentiles of senior tranche coupon are 5.9%, 6.0%, and 6.2%, respectively. The 25th, 50th, and 75th percentiles of mezzanine tranche coupon are 6.6%, 7.5%, and 9.7%, respectively.

The mean, 25th, 50th, and 75th percentiles of the available coupon of each rating category (includes +/-) can be found in the table above.

II-C. Tranche Spread Analysis

The average spread (over 3 months SOFR) of senior tranches and mezzanine tranches are 1.4% and 3.8%, respectively. The 25th, 50th, and 75th percentiles of senior tranche spread (over 3 months SOFR) are 1.3%, 1.4%, and 1.5%, respectively. The 25th, 50th, and 75th percentiles of mezzanine tranche spread (over 3 months SOFR) are 2.0%, 3.0%, and 5.5%, respectively.

The mean, 25th, 50th, and 75th percentiles of the available spread (over 3 months SOFR) of each rating category (includes +/-) can be found in the table above.

II-D. Egan-Jones Ratings vs Other Agencies

Below is a summary of Egan-Jones ratings compared with other agencies. For the detailed full listing and sorting of Egan-Jones’s CLO ratings, please visit our website at https://egan-jones.io/non-nrsro-ratings/clo.

Egan-Jones's Key Rating Features & Differences Compared With Others

Below is a summary of Egan-Jones's approach (see our Methodology for a more complete description):

1. Our rating is derived from estimated losses.

2. The probabilities of default utilized are generally more conservative than industry standards.

3. Generally, our ratings are more heavily model-driven and take into account fewer subjective assumptions.

4. Generally, we update the cash flow and ratings monthly based on the availability of the trustee reports.

5. Our analysis is conducted using information and cash flow engines supplied by a recognized industry provider.

6. For some transactions, when senior tranches are being paid down/off, our ratings on subordinated tranches generally move higher than the initial rating due to the improved tranche subordination and resulting in less estimated loss. To avoid confusion, we exclude from the chart above the impacted transactions. (AMMC 2016-18A, ANCHF 2016-3A, ANCHF 2016-4A, ANCHF 2019-9A, ANCHF 2020-10A, ANCHF 2020-12A, ANCHF 2022-15A, APID 2015-22A, APID 2017-26A, ARES 2018-49A, BALLY 2021-18A, BCRK 2015-1A, BRIST 2016-1A, BSP 2016-9A, CANYC 2012-1RA, CATLK 2015-3A, CGMS 2013-1A, CIFC 2017-4A, CLRCK 2015-1A, DCF 2021-4A, DRSLF 2017-47A, FLAT 2018-1A, GALXY 2015-21A, GCBSL 2019-43A, GOCAP 2015-26A, HLA 2015-3A, HLA 2017-1A, HLA 2017-2A, HLM 11A-17, ICG 2014-2A, JMP 2017-1A, KKR 13, KKR 18, KKR 9, LCM 15A, LCM 38A, MAGNE 2018-20A, MCLO 2015-8A, MORGN 2018-2A, MP10 2017-1A, MP8 2015-2A, MVEW 2017-1A, WELF 2017-2A)

III. Pool Asset Key Metrics Summary

This section summarizes the characteristics of the underlying loans in the CLO deals.

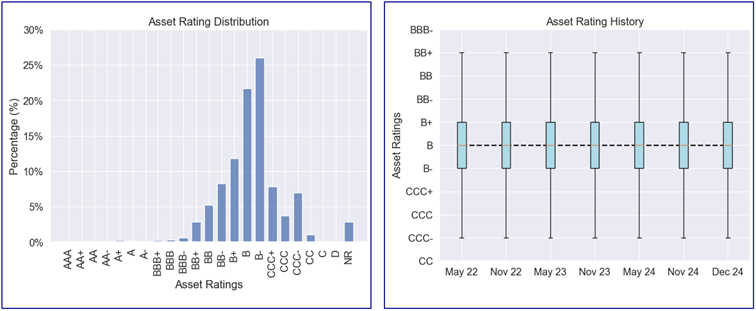

III-A. Asset Distribution

III-B. Asset Coupon Analysis

III-C. Asset Rating Analysis

III-D. Asset Default Analysis

Footnotes and sources

- https://finsight.com/collateralized-loans-clos-abs-bond-issuance-overview?products=ABS®ions=USOA

Adj asset coupon means gross asset coupon minus the asset estimated losses which is assumed 50% of loss given default.

Weighted Average Rating Score is derived from a 10-year default rate and used to calculate the weighted average default probability of the portfolio.

Diversity Score represents the number of independent, identical assets that we can use to mimic the default distribution of the actual portfolio.

Tranches Subordination is calculated as (Collateral Value - (Pari-Passu Balance + Senior Balance)) / Collateral Value. Defaulted assets are valued at market value.

For more details, please refer to Egan-Jones's CLO methodology.